Match Group one year later: a cash cow stuck in the mud

And how AI won't save a lacklustre product roadmap

Introduction

In March of last year I wrote an extensive report about why I thought Match Group was undervalued at those levels (ca. $33 when I published my first report). A (fiscal) year later the company is trading at pretty much the same price (ca. $34 at the time of writing).

With an FCF yield of nearly 10%, it resembles a fat cow happily grazing in the meadow and producing good milk, but almost ready to be taken to the slaughterhouse. That slaughterhouse can take the form of a private equity shop or other tech giant that decides to take it private.

Most of the issues as well as potential opportunities that I covered in my previous report are still intact, and, as such, I still think at this level Match Group remains a fairly good value play. However, there are several areas that make me less optimistic than I was a year ago.

Management is confident they will be able to deliver positive results in 2025 thanks to their marketing and product plans and increased operational efficiencies. While I think there is still a lot of room for improvement in terms of efficiencies and cost cutting, I’m very sceptical about their product roadmap. Based on what I’ve seen during their investor day presentation last December, I believe the company has fallen prey to the AI hype and is trying to incorporate it in any possible way in their product roadmap.

While AI's potential for increasing workflow productivity within the firm is undeniable, I believe, at this stage, AI is more of a buzzword used in earnings calls to placate analysts rather than a concrete solution for enhancing user experience in the dating space.

I’m a firm believer that when it comes to relationship or connecting to people in general, AI is not the answer.

While the nature of the dating industry means that early movers like Match Group have cemented a competitive position that is difficult to undermine, the risk of operating in a de facto duopoly is the potential to become complacent regarding what people truly desire. With direct impacts to product innovation.

Stagnating growth in a complex macro environment

Match ended 2024 with $3.5B in revenue, up 3% y/y, and an operating margin equal to 26%, a couple percentage points higher than the previous two quarters.

Source: Match Group Q4 2024 Presentation

Margin expansion during the year is mainly attributed to the Power of the Portfolio Plus initiative, that aims to operate more effectively as a connected portfolio of brands.

The concerning aspect is that its main brand Tinder might have plateaued, as shown by the slightly decreasing top line, but most importantly by the dynamic with payers and revenue per payer (RPP).

Source: Match Group Q4 2024 Presentation

In the Q4 2024 executive summary, management’s comments that they “do not expect any one product initiative to have a material user or revenue impact, but that over the course of 2025 and beyond, we believe Tinder’s planned product initiatives will steadily enhance the user experience.”

Translated: they have no clue what to do with Tinder (more on this later).

What is keeping the company afloat is Hinge’s global expansion progress. Through mid-January, Hinge was the #1 most downloaded dating app in 10 countries and remained the #2 app across Western Europe2 (source: Sensor Tower). Hinge plans to expand into Mexico and Brazil in the second half of 2025, as it looks to expand beyond core English-speaking and European markets.

Nevertheless, Hinge currently represents ca. 16% of total revenue at Tinder, and it derives less than 10% of its revenue from Europe. This shows the opportunity for Match to have a much bigger business at Hinge in these European markets.

While there is still ample room for growth, key metrics are showing some signs of inflection.

Source: Match Group Q4 2024 Presentation

Moreover, there is the real, unquantifiable risk of cannibalization between the two apps. Translated: if Hinge continues or even accelerates growth, that might not translate to additional total revenue for the whole group.

Finally, Evergreen and Emerging brands recorded a 7% decline in revenues. Contrary to Tinder and Hinge, the company doesn’t even mention potential top line accretive product initiatives, but rather focuses on driving efficiencies by migrating to a shared/centralized operational and organizational platform (“build once, deploy everywhere”).

Consolidating evergreen brands into a single platform will drive efficiencies and enhance focus. The fact that they also discontinued live streaming services and decided to sunset Hyperconnect’s Hakuna app, shows they are not focused on growth at all costs but rather on building a rational portfolio of apps that can increase margins.

However, there doesn’t seem to be any significant traction among the newest apps (such as Chispa, BLK and Salaams, which focus on Hispanic, Black and Muslim communities, respectively), and for now their contribution is only offsetting the decline among evergreen brands (such as Match.com, Plenty of Fish and OKCupid).

Source: Match Group Q4 2024 Presentation

The only positive note that I can find when looking at Match Group’s revenue numbers is that people underestimate the impact of Fed rate cuts: a weaker dollar has a massive impact on Match as a great share of their business is abroad, but they consolidate in $. For context, revenue grew 4% y/y in Q2 of last year, but it was up 8% on a foreign exchange neutral basis.

However, this potential tailwind was supposed to materialize already in 2024, and the prospect of a ‘stronger for longer’ dollar makes this assumption less strong.

For full year 2025, management expects to deliver total revenue of $3,375 to $3,500 million, down 3% to up 1% Y/Y.

Gen Z is tapping out and price increases may soon hit a wall

Price increases across the whole portfolio have allowed Match’s top line to increase slightly in the past few quarters and have more than compensated for the decreasing number of paying users.

Europe's economic situation is poor, and a recession could follow by the end of the year. Some argue that dating apps are non-essential, and as inflation and/or weak economic growth pressures consumers, stocks like Match would suffer.

However, I don’t think the price elasticity has been figured out for dating apps yet. In the wake of the 2008 recession, dating apps held up pretty well compared to other non-essential items. However, back then dating apps were just a nascent trend and as such not really comparable. If we end up having a recession in the near future, this will tell where dating apps stand in the consumption pyramid.

Match’s Revenue Per Payer (“RPP”) across all geographies increased 3% to $19.29 in 2024. Bumble’s average revenue per paying user (ARPPU), on the other hand, was $25.58 in Q3, a ca. 35% premium to Match. While there are differences in dating intent, demographics (notably age and income) and potentially geographic mix differences that may explain some of the delta, the large gap does signal an opportunity for Match to get traction with price increases.

However, Bumble’s ARPPU was $28.38 a year earlier. This strong slowdown signals there might be a cap to how much dating apps can expect to extract from users.

Match Group’s management has reiterated many times during earning calls that their primary focus is on maximizing revenue, and not specifically RPP or payers. Yet, trends among younger generations are shifting.

Millennials, the nation’s largest generation, were prime dating age when Tinder first rolled out, but as they grow and marry and quit dating apps, Gen Z is now becoming the primary user: a younger, and smaller demographic with less disposable income. That generational shift poses a challenge for the dating app industry.

Product developments don't justify the billions spent over recent years

Product strategy can sometimes feel like a nebulous practice whose drivers of value are difficult to quantify when it comes to the bottom line.

From 2021 to 2024, Match spent approximately $1.3B on product development. Product development costs increased 12% Y/Y in Q4, representing 13% of total revenue, up one point Y/Y.

Still, there's been very little added to any platform and no significant improvement in the user experience.

While new Trust&Safety features at Tinder were helpful in shedding unwanted users from the platform and improving the overall experience, other than that I don’t see any exciting feature coming up soon. Management noted the following during the last earning call:

“Match Group has activated several teams across our brands to begin working on applying the latest AI technologies to help solve key dating pain points. These teams have been able to rapidly develop new features, with a number of initial features expected to launch over the next two quarters. These include helping users select their optimal photos and leveraging AI to highlight why a given profile may be a good match.”

Select their optimal photo??? Highlight why a given profile may be a good match?? Is this the best they can do with all the $$$ spent on product development???

I think people crave more novel dating experiences, and none of this seems novel enough to get me excited…

During the first investor day last December, the company announced it will unveil some promising advancement related to product development, and in particular with regards to the use of AI to enhance the user experience, increase penetration and win back lapsed users.

The approach to product and AI seems to be taken from a consultant delivering their final presentation to the board: devoid of substance and full of buzzwords.

Source: Match Group Investor Day – Dec 2024

Take the example of Tinder. The brand has been suffering for several quarters with stagnating growth and declining MAU. How are they going to fix it? We don’t know, but rest assured that ‘AI is the next revolutionary unlock.’

Source: Match Group Investor Day – Dec 2024

So, what have the ACTUAL product innovations been?

The AI photo finder?

Source: Match Group Investor Day – Dec 2024

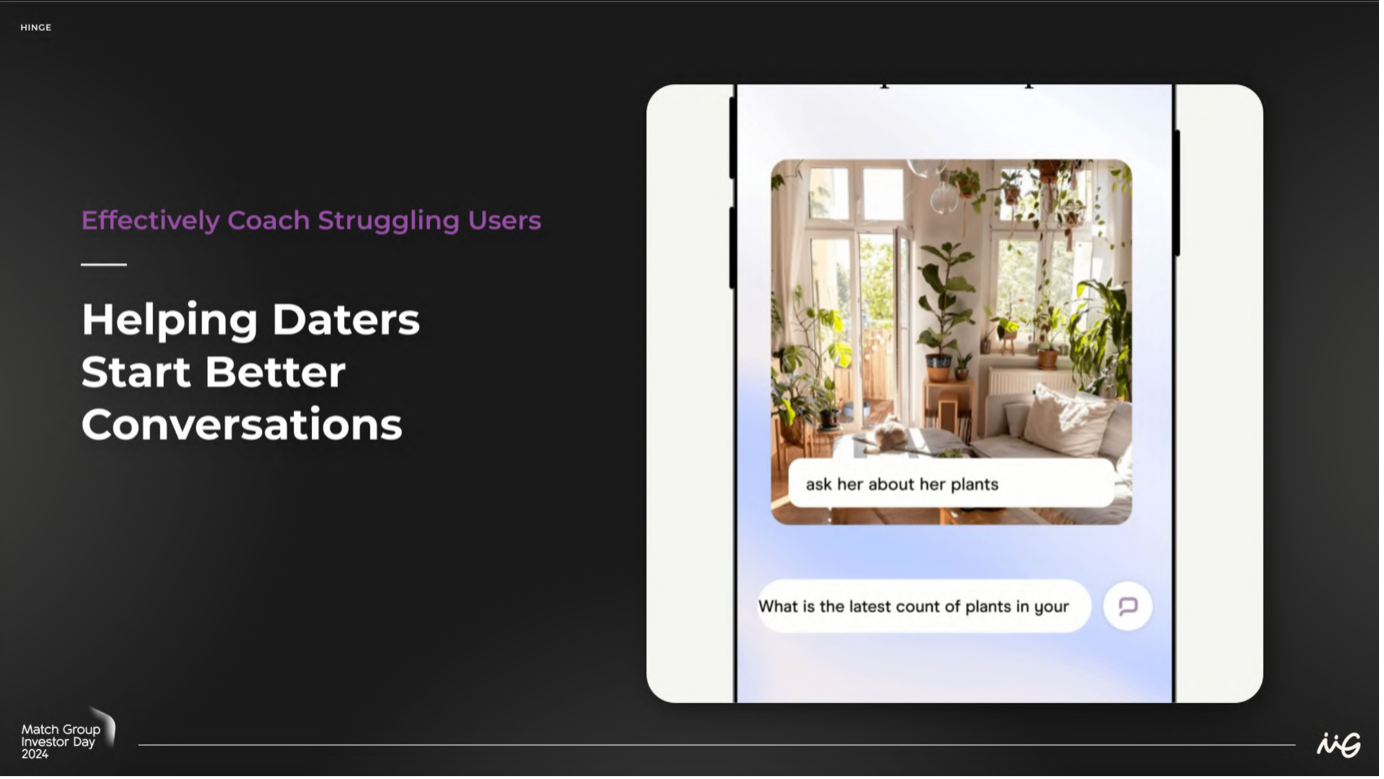

Or prompting users to ask their matches about their plants…?

Source: Match Group Investor Day – Dec 2024

All in all, the product roadmap for Tinder doesn’t show anything exciting.

Source: Match Group Investor Day – Dec 2024

This is simply not acceptable for a company that has spent $$$ in product development.

AI is not the answer

As I wrote back in March of last year, people don’t want to add more ‘artificiality’ to what is already a very artificial experience. We are not wired to select our mates and friends by swiping and scrolling, but rather by interacting in person, smelling, touching, talking. We crave human connection, not artificial connection.

I think that trying to fit AI in whatever way possible inside the product roadmap is the wrong approach.

I was browsing for events in Los Angeles on Eventbrite a few days ago and noticed that many revolved around matchmaking and speed dating. Many of them had a ticket price of $50+ and were already booked out.

I don’t know the economics of these events, but I can sense that the stigma around these types of events is diminishing, and that people would rather risk embarrassment and interact in person rather than spend hours in front of a screen feeling nothing.

While throwing live events would pose challenges in terms of scalability, as well as likely be margin dilutive for a public company like Match, there is an unquestionable appeal about connecting offline, rather than through a screen.

Meeting people in person is becoming an enticing option for those experiencing app fatigue. Companies have taken notice and are leveraging this in their products. Last week I got this in my inbox from Classpass.

And some are capitalizing on this trend by building products that serve as facilitators for making connections outside the app.

For instance, London-based startup Thursday markets itself as the ‘offline dating app.’ The app is available only on Thursday; when the clock strikes midnight, users toggle an icon to indicate that they’re ready to date that day. For the next 24 hours, they can swipe and chat as on other dating apps. However, when Thursday becomes Friday, their matches disappear and the app locks until next Thursday. The implication is that there’s no time to waste with chitchat. They also organise members-only, IRL events/mixers where people can connect.

Thursday’s website homepage

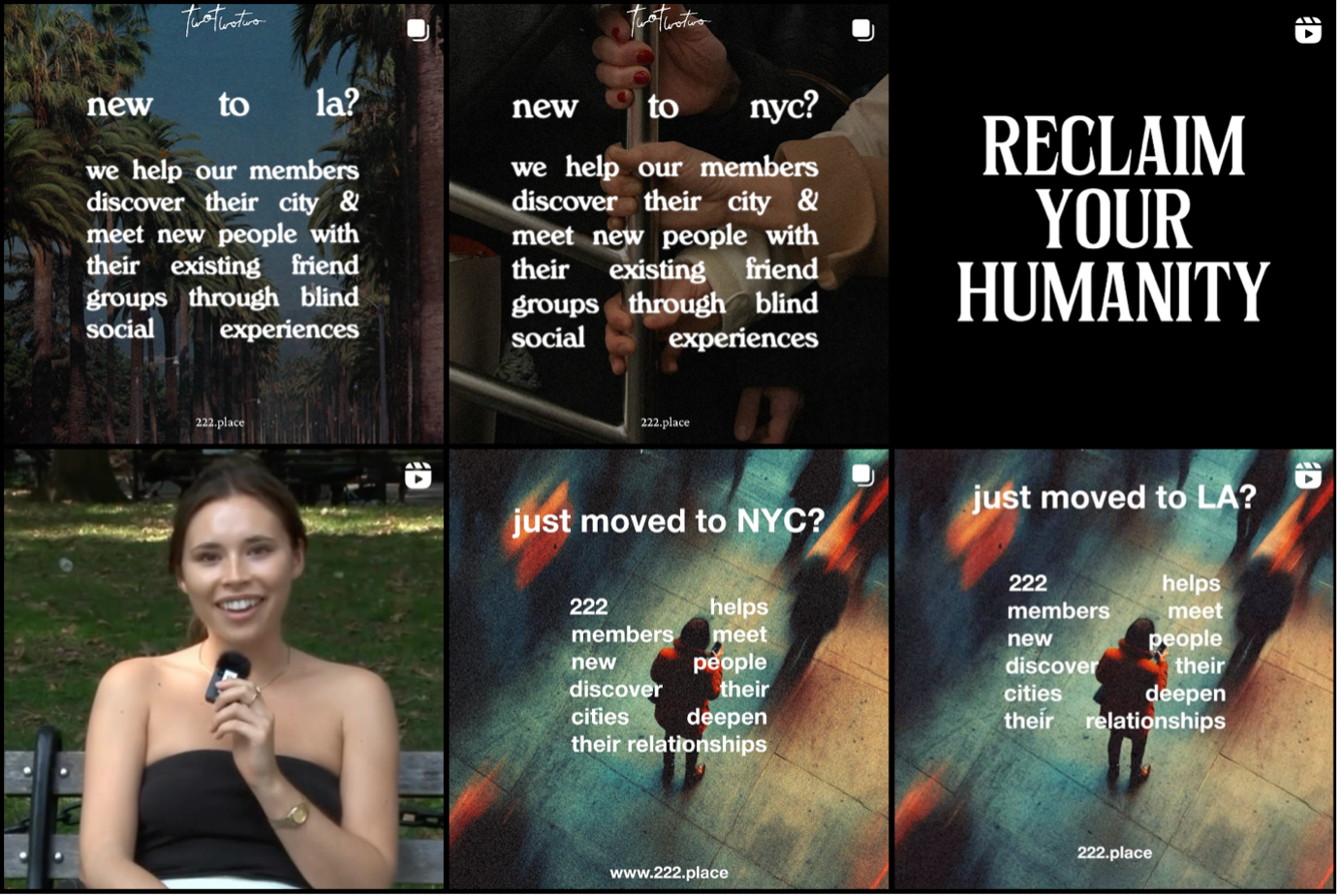

Los Angeles-based 222 operates in a similar fashion, but with a focus on friendship and connection rather than dating. They created a marketplace between hyperlocal venues and members looking to discover their city and meet new people through unique social experiences. “no profiles, no DMs, no scrolling, no swiping. Just say “yes” & explore the chance encounters you'd have never experienced.”

A screenshot from 222’s Instagram page. The app brands itself around ‘reclaiming humanity’.

Similarly, Paris-based Timeleft matches users with strangers for dinner via a personality algorithm. Dinners are currently held around the world on Wednesday and the app helps with the matching, logistic, as well as provide icebreaking games and an ‘after-dinner drinks’ location that only unlock one hour after dinner starts. On the Tuesday before the event, people receive a brief introduction about their fellow diners.

Timeleft’s flow to participate to an event

I did some research on Reddit to understand the feedback about these new apps from people who tried them, and the majority of the reviews and comments were very enthusiastic.

I believe Match could benefit from incorporating features or even developing dedicated apps that replicate some of these mechanics, thus providing an alternative to traditional app-based dating.

Now, I’m not suggesting Tinder and Hinge become a speed dates organiser, but between relying on AI as the sole driver of innovation and bringing people together IRL, there is a lot in between that can be activated to improve the experience.

There is a reason why Match has not ventured into this space, and it's because it is a public stock and, as such, it has a gun pointed to its head when it comes to cashflow generation and margins.

I don't think anything will disrupt Tinder and Hinge and the other traditional matchmaking apps any time soon, but the time is ripe for new players to take away fractions of their business by introducing an experience that is more human. The question for these players remains how to scale something that is by definition difficult to scale.

Share buybacks continue to be diluted by increasing stock-based compensation

For the full year 2024, Match repurchased 22.2 million shares of common stock at an average price of approximately $34 per share on a trade date basis, for $753 million, representing approximately 85% of 2024 FCF.

Still, Operating Income in Q4 was $223 million, down 14% Y/Y, impacted by increased stock-based compensation expense due to higher headcount and lower forfeitures of equity awards in 2024 than in 2023.

Since resuming their share repurchase program in May 2022, Match has used more than $2 billion of cash to repurchase an aggregate of ca. 40 million shares.

Source: Match Group Q4 2024 Presentation

However, as of Q4 2024, diluted shares outstanding have only decreased by ca. 30 million compared to Q1 2022, while stock-based compensation continues to rise.

SBC was equal to $232 million in 2023. According to management forecast, it will increase to $305 to $315 million in 2025, or 9% of forecasted revenue (it was 4.9% in 2021). For context the average for Apple, Microsoft, Alphabet and Amazon is ca. 3.5% (at the time of writing).

Marketing efforts are still a question mark in terms of ROI

Marketing spend in 2024 was down one point Y/Y as a percentage of total revenue to 17%.

While marketing is possibly supporting growth at Hinge (especially in Europe) while trying to shuffle the hookup stigma about Tinder, it is a big chunk of revenue that needs to bring more solid results in terms of both overall users and revenue. While they seem to be aware of it (“We fully recognize though that if the top line growth does not materialize as we expect, we'll need to consider all options, including reduced investment and other alternatives. That said, we remain very confident that we're on the right track.”), this has been the narrative for a few quarters now, and unless they can turn it around and achieve a higher ROI on their marketing spend, it becomes a problem. If you product innovation is already shaky, overspending in marketing is only a temporary band-aid.

CEO shakeup

A few quarters ago, I wrote on Twitter (X) that I'd recommend listening to a Match conference call instead of reading a transcript. The scripted, monotone discussions between analysts and the at the time CEO Bernard Kim gave me second thoughts about whether or not he knew what he was doing.

While I don’t question Bernard Kim’s track record, he started to feel like a broken record, repeating himself many times now quarter after quarter.

In this sense, the appointment of Spencer Rascoff didn’t come as a surprise. Rascoff joined as a member of the board in March 2024, after activist investor Elliott Management acquired a $1B stake in the company.

The departure of Bernard Kim was decidedly abrupt, which in my opinion signals how the board was dissatisfied with the lacklustre performance and lack of tangible product innovation.

Rascoff is a serial entrepreneur (he founded Hotwire, which was sold to Expedia in 2003, and Zillow, which IPOed in 2011) and, most importantly, was already on the board of directors and already knows the team, the strategy and the metrics he will be working with.

Unlike Bernard Kim, whose scripted, monotone conference calls would make you cringe and beg for a break, Rascoff seems to be at ease when speaking to analysts, to the point where during the earning call last week he even reminisced with an analyst present on the call and addressing a question to him about metrics discussed with him during his time at Zillow.

Conclusion

Match is expecting top line revenue to decrease low single digit in 2025, or in the best-case scenario to stay flat. It will continue to print cash at the tune of $1B, which it will mostly use to reduce the number of diluted shares outstanding.

Source: Match Group Q4 2024 Presentation

Last year I predicted that they would introduce a dividend.

Last December they announced a $0.19 quarterly dividend (or ca. 2% yield at current prices).

The market was not excited, although during the same they disappointed with a bland product roadmap. However, I wrote several times that this fetish with growth at all costs is overrated, in my opinion. Match is in a different phase of its lifecycle: it is not a growth stock anymore and the market needs to come to terms with it. Match is printing cash, and management clearly doesn’t know how to innovate anymore in a market that is craving real in person connections rather than digital ones. Returning money to shareholders via dividends and buybacks is the most logical thing.

Match currently holds $3.9B in long-term debt on its balance sheet, a part of which will need to be refinanced at higher rates in the near future. I believe that being more conservative with regards to SBC will free up funds allocated to share buybacks to lower the debt load.

Elliot and other active hedge funds have amassed a considerable stake in the company. Elliot owns roughly 10% of the company (at current market capitalization), and just as it has pushed for the introduction of a dividend as well more rigorous SBC management and share buybacks, it will possibly push to sell the company or take it private.

Jennifer Saba from the Wall Street Journal made the math pretty easy a few months ago:

“Including debt, Match was valued at around 26 times expected EBITDA in early 2022; it now trades at 9 times. Assume a buyout shop offered a 25% premium, for an enterprise value of some $14 billion. Strip out stock-based compensation, and EBITDA should be slightly over $1 billion. Banks might offer six times that in debt, leaving a bit more than half the purchase price to fund with equity. That’s punchy, but just about plausible, especially if current shareholders like Elliott join in.”

Disclosure: I have a beneficial long position in the shares of MTCH either through stock ownership, options, or other derivatives.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it and I have no business relationship with Match Group.

This is not financial advice. Do you own due diligence.